US-Iran War: Ceasefire Now... What's Next?

Investment Navigator, April 2026 Edition

Is this truce a turning point towards peace, or just a pause?

With US-Iran tensions still simmering over differing strategic objectives, will the 14-day ceasefire hold, or will fresh provocations plunge the region back into chaos?

Has the stagflation threat peaked?

Markets welcome the ceasefire, but concerns over a constrained Straits of Hormuz remains. Shortages in key areas such as gas, fertiliser and helium threatens to push prices higher. How will central banks respond?

Where are the opportunities in the aftermath?

Asia endured the brunt of the shock, while precious metals also sold off until most recently. With the latest ceasefire development, how and when should investors risk on?

In this Investment Navigator – April 2026 edition, we discuss whether the ceasefire’s relief rally can last, how supply chain bottlenecks could reshape inflation, and why diversification is more critical than ever.

📈Market heaves a sigh of relief on a two-week ceasefire

The announcement of a two-week ceasefire on the 7 April between the United States and Iran marks a critical, albeit tentative, shift in the ongoing Middle East conflict. This temporary cessation of hostilities is strictly conditional upon the reopening of the Strait of Hormuz, a vital artery for global maritime trade that has been choked by the recent war situation.

Markets reacted positively to the news, breathing a huge sigh of relief as the war entered a sixth week and was looking to further escalate. Equities market rallied, with the S&P 500 marking one of its best sessions since a year ago, triggered by a 15% drop in oil prices (largest one day decline since 2020). We see this as a move in the right direction, although the underlying sentiment remains one of extreme caution, and the road towards peace and stability remains inherently fragile. The next 14 days following this announcement will serve as a high-stakes litmus test for both nations' commitment to de-escalation, as any minor provocation could shatter the current calm and send the region back into chaos.

🕊️The start of a long road towards peace

It is important to recognise that the agreed upon ceasefire is strictly limited to a 14-day window, serving primarily as a necessary political and economic off-ramp to alleviate immediate global pressures. It is not a definitive armistice or a permanent end to the war. The core strategic conflicts remain entirely unresolved. The US objectives, centred on regional stability and nuclear non-proliferation, remain largely at odds with Iran’s position on sovereignty and the removal of crippling economic sanctions.

The underlying framework for future negotiations, ostensibly based on a 10-point proposal, involves highly contentious demands regarding the permanent control of maritime navigation, the future of the Iranian nuclear program, and the comprehensive lifting of sanctions. The profound disparity between the strategic objectives of the involved parties suggests that navigating a permanent resolution will be exceedingly difficult, leaving the region highly susceptible to renewed volatility once the temporary truce period ends. Achieving long-term peace remains an uphill battle, and negotiations scheduled following the first meeting gives a glimmer of diplomatic hope that the conflict could transition from military posturing to dialogue

Read more about our stance on the Middle East conflict through the Investment Strategy Focus April 2026 .

🚢The logistical reality of reopening the Strait

The physical reopening of the Strait of Hormuz is vastly more complex than a simple political declaration. Maritime mines suggest that a safe passage through the strait must be highly coordinated with the Iranians. Additionally, there is currently a severe backlog of more than 800 vessels remaining trapped or idle in the Persian Gulf region, and resolving this bottleneck will require considerable time given the capacity constraints of the narrow waterway. Beyond the physical clearing of the waterways, the oil supply shock will take significant time to rectify, as production facilities that were mothballed or damaged cannot return to full capacity overnight. It will take months before the supply normalises.

Global markets must therefore brace for a substantial lag between the political agreement to resume trade and the actual physical arrival of tankers at their destinations. Furthermore, there will undoubtedly be an increase in shipping premiums for sailing through the strait, and we are also witnessing emerging indications that Iran may attempt to leverage the situation to implement new, structural transit fees. Such measures would permanently alter the cost dynamics of global maritime trade in the region, which may in turn keep energy prices volatile in the immediate term. Our near-term target for Brent remains at $100/barrel.

🚩The threat of stagflation is still increasing

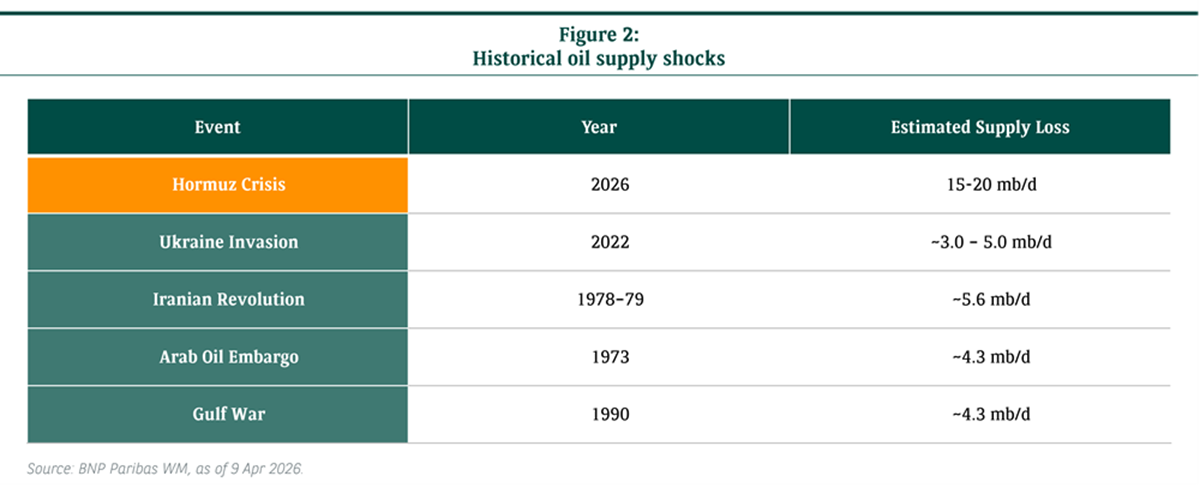

The disruption due to the conflict is now officially the largest oil supply shock in history by volume (see Figure 2). Compared to previous significant supply shock events, where on average the estimated supply loss is approximately 5 million barrels a day (mb/d), the 15-20 mb/d loss (which accounts for roughly 20% of the global oil demand) affected by the closure of the Strait of Hormuz is massive, given there are few viable alternatives to bypass this route. In the short term, Saudi pipelines to the Red Sea, UAE alternative routing, floating oil, sanctions relief and strategic petroleum reserves (SPR) releases is getting the shortage down to 7-10 mb/d, but the clock is ticking.

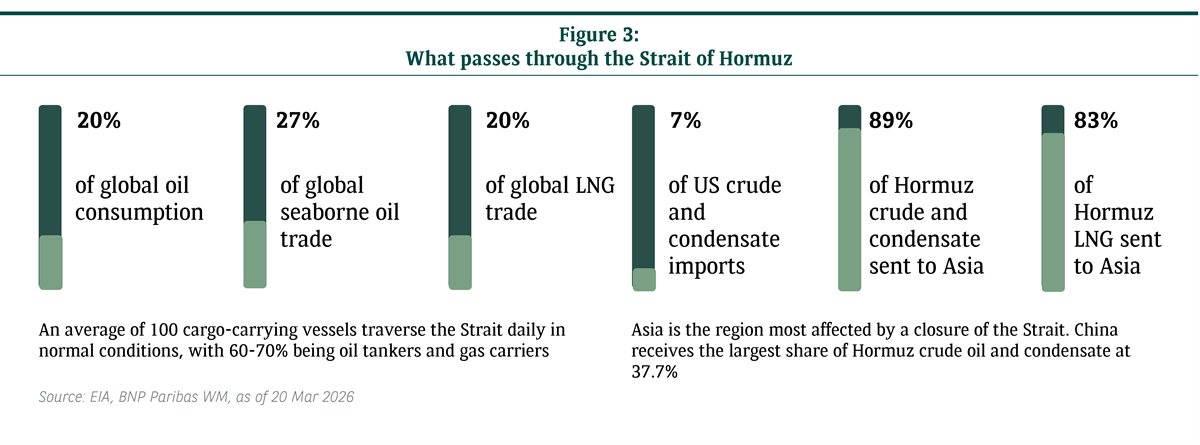

The global economy is now grappling with the impact of a longer-than-anticipated disruption in the oil supply. In fact, given that the oil tankers typically take more than a month to reach Asia from the Middle East (89% of Hormuz crude and condensate is sent to Asia, see Figure 3), the East is only now beginning to feel the price pinch. Going forward, the key to stabilising oil prices will be determined by the pace of reopening the Strait of Hormuz and how quickly supply can be restored to pre-war levels. Of course, this also hinges on no further escalation to the current ceasefire.

Beyond oil, the conflict has also resulted in significant reduction of exports in key areas such as natural gas, fertilisers and helium. Qatar alone accounts for 20% of global natural gas supply as well as 30% of the world’s helium, which is indispensable for cooling MRI machines and manufacturing advanced semiconductors for AI infrastructure. The region also accounts for nearly one-third of global nitrogen-based fertiliser trade. Disruptions in April, the peak Northern Hemisphere planting season, threaten global food security. Unlike oil, these specialised materials have almost no alternative transit routes or spare global capacity and could further drive inflation upward.

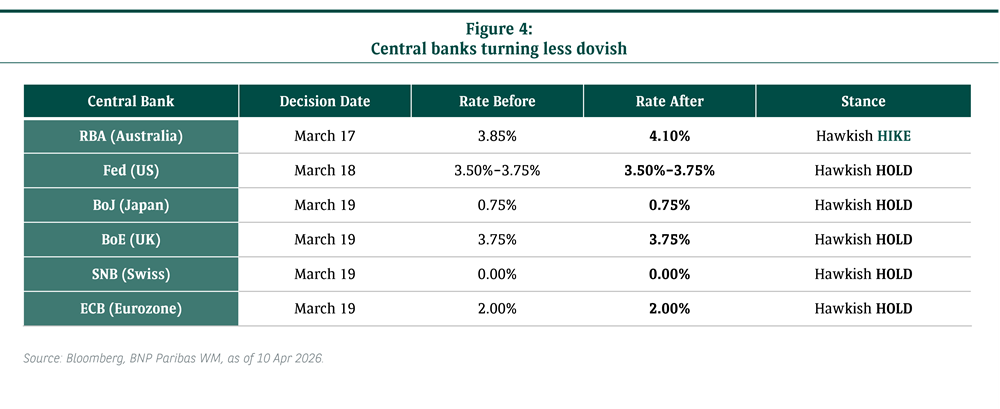

Inflation expectations have picked up, and in response, central banks around the world have started to pivot slightly away from their initially dovish stance, with some even suggesting increasing interest rates to combat rising costs despite the risk to growth. The recent diplomatic developments mark a crucial step away from a severe tail-risk event. Hence, the risks to a prolonged inflationary shock have declined in a meaningful way. This should ease the pressure on central banks in the near term and allow most to adopt a wait-and-see approach. For the Fed, we now expect no further rate cuts this year (from one cut previously), given the upside risk in inflation and a more balanced labour market. For the ECB, we think they will likely remain on hold this year, albeit the risk of a hike towards the end of this year has increased considerably.

🧭Navigating near term volatility

As we look ahead, market volatility could return as tensions could flare yet again, especially given the fragile nature of a ceasefire. Moreover, the longer-lasting impact on global growth and earnings still needs to be evaluated. While the world certainly became a more friendly place to carry risk, the underlying market environment remains characterised by elevated geopolitical uncertainty.

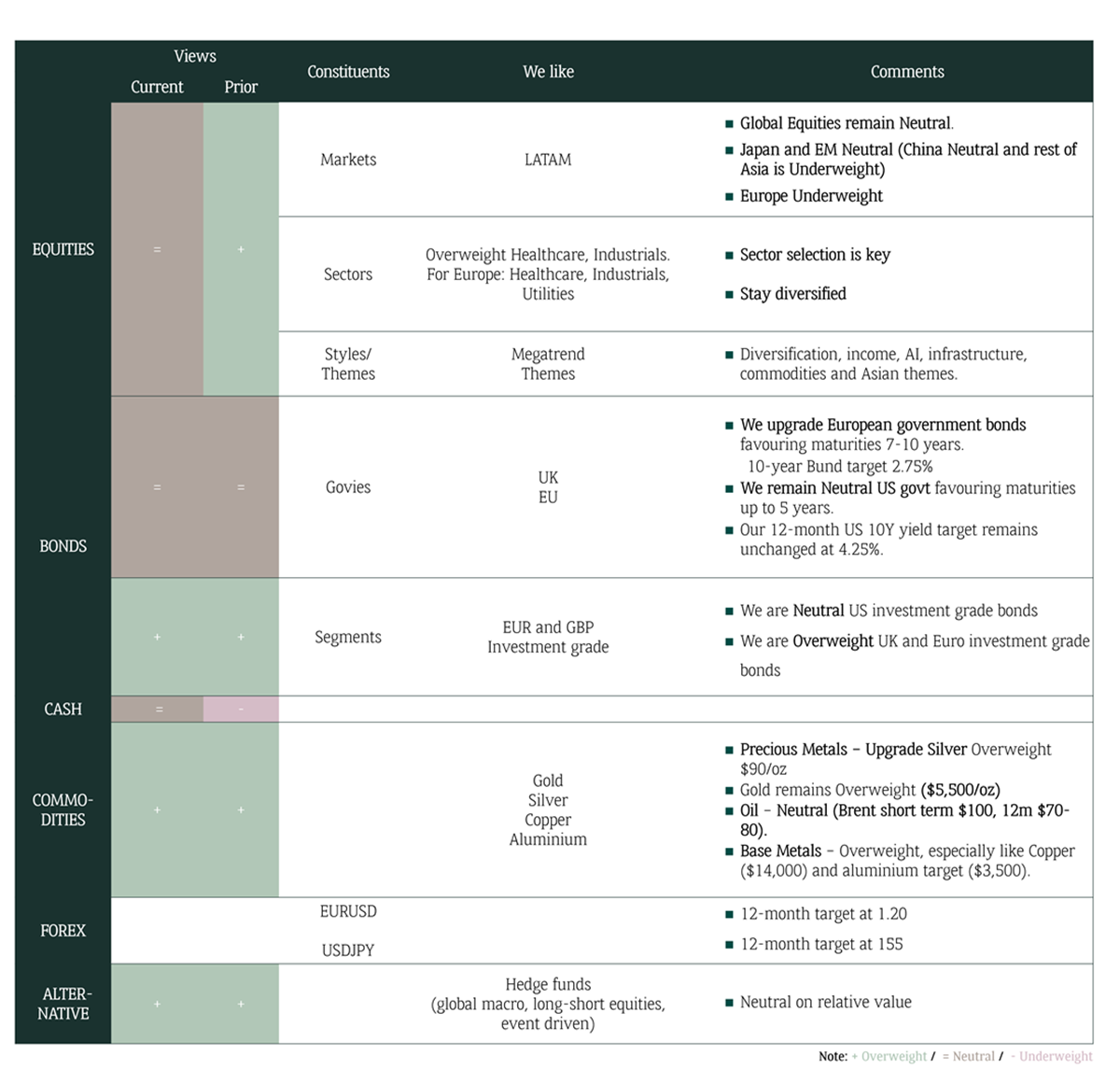

Therefore, we confirm our Neutral view on equities for the time being. However, due to the decreased downside tail risks, we would not fade the rally at this point in time. We will be carefully monitoring the diplomatic developments over the coming weeks. Before taking on any additional risks, we need a higher degree of clarity about the durability of any (new) agreement because this will be decisive in shaping the medium-term risk landscape, the trajectory of global inflation, and the corresponding monetary policy outlook.

At this juncture, we continue to advocate for a diversified portfolio, with a tilt towards value and defensive for equities. The trend of diversification away from the dollar should resume post-conflict given the likely diversification away from the petrodollars amongst the Gulf Cooperation Council (GCC). The weaker dollar and the possibility of higher inflation (and hence lower real rates) are supportive of gold prices, and we stay Positive with a target price of USD 5,500/oz, while also upgrading our silver view to Positive from Neutral (target price: USD 90/oz). That being said, investors should also continue to prepare a potential buy list of opportunities to act upon if the cloud of uncertainty subsides further. The worst-hit areas (Asia in particular) are likely to benefit the most if we achieve a credible conclusion to this conflict.

Click HERE to discover the answers to the frequently asked questions on Middle East conflict from our clients.

Overview of our CIO Asset Allocation for April 2026

Please read carefully the disclaimer: https://bnpp.lk/-asia-disclaimer